Geothermal Heat PumpsWFI makes geothermal heat pumps. Wikipedia article describes history, principles that underlie the technology, how the technology works, economics. WFI's former president Bruce Ritchie explains in this video how it works and why it is so worthwhile.

Industry Prospects

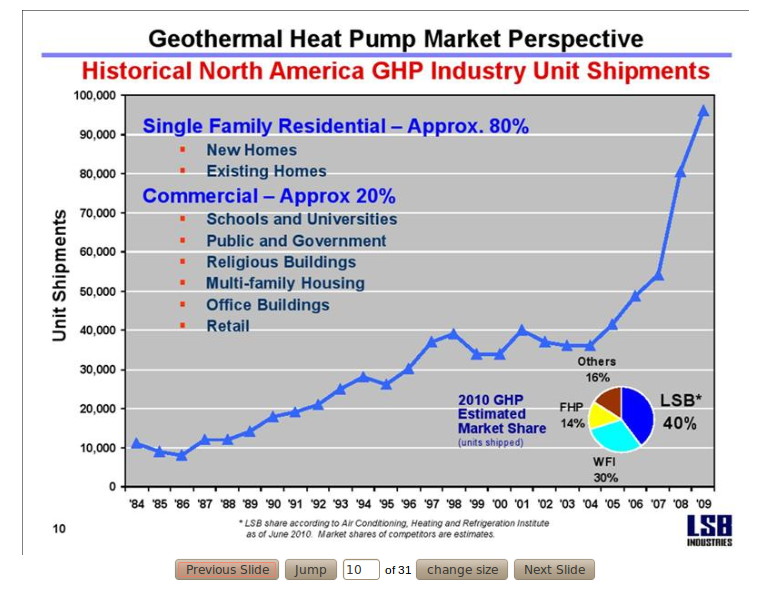

Presentation by LSB Industries at Canaccord Genuity Conference 10th August 2010

Geothermal Maturity

- technology for energy known for many years, proven efficiency benefits; manufacturer equipment still improving but fairly close in technical capability - key differentiator for install success is contractor installer skill and diligence

- dealer networks in place, extension of capability for contractors

- consumer knowledge in North America in its infancy but the information/hype infrastructure is in place - industry associations (GeoExchange in USA, Canadian GeoExchange Coalition), web sites and consumer forums (GreenBuilding Talk)

- residential easiest and cheapest for new-build but still attractive for retrofit, esp. at furnace or air con replacement moment; WatwerFurnace claims present 100k annual install rate could rise to 1 million p.a. by 2016

- attraction is fuel bill savings, appreciable now and probably greater in future if commercial aka power company prices rise

- government tax breaks and write-offs are an incentive

- substantial up-front cost creates affordability challenge, especially at a time when home values are dropping, credit is tight and consumers are trying to reduce debt, not take on more

- lack of knowledge and solution visibility and trust not quite there - are we close to a tipping point?

Market Growth:

- stalled during housing crash in USA - housing starts down to 500k annually but WaterFurnace expecting (Q2 earnings call) return to 1.2 -1.5 million p.a. by c. 2012

Competition

- main competitor is LSB Industries (NYSE: LXU), which has about twice the $ sales of WFI in climate control, though the manufacturing figures of the US Energy Information Administration for 2008 has them about equal in shipments (WFI = Indiana, LXU = Oklahoma); WFI has gained market share in 2010, as it claims in its 2Q Report - its sales rose 13% in the first six months of 2010 while LXU's fell 11%;

- biggest other competition - Trane (owner Ingersoll Rand), Florida Heat Pump (owner Bosch), McQuay (owner Daikin of Japan), Mammoth (private company)

- October release of shipment figures by the US EIA will show evolution of market share through 2009

WaterFurnace the Company and the Stock

Visibility: Not Just Under the Radar, It's Well Below Ground

- Low trading volume - 11,000 average but in recent months even lower; trades are in small amounts, 1 or 2 board lots at a time, indicating retail investors, not institutional investors are the market

- Google Finance does not even track price now - trading volumes too low?

- Only two analysts cover it

- Only a few Globe and Mail stories - mostly in stock screens results for desirable traits

- US interest low - likely because it is a US company traded in Canada on TSX

- not listed in StockChase, no chat board on Raging Bull etc

- no search results on book website for Clean Tech Revolution, nor is it mentioned in the book; not in book Investing in Renewable Energy nor is it in a search of that book's website Green Chip Stocks

- boring - uggh, they make HVAC equipment; ughh, stock price hasn't budged in four years; also likely means that "momentum" traders are staying away, so we shouldn't expect big leaps and swings; boring is good

- Cormark Securities has a full stock investment assessment on Power and Alternative Energy Companies that includes WaterFurnace; 12 mth price target is C$31 based on historical average P/E and projected EPS in 2011

- warranty costs - WFI mgmt assumes constant failure rate according to historical experience; has a long enough track record to assess the 10 year warranty it offers but new products may not do as well (any ISO quality control for manufacturing or by its chosen supplier partners?)

- margin pressure due to

- material costs, esp copper tubing, rising faster than price increase can compensate, together with

- competitors, who are in most cases, as Company docs say, larger and can source raw materials cheaper; 2Q earnings call mentioned drive to expand market share as successful but at cost of lower margins; same call mentions that it has taken steps to improve efficiency (outsource some manuf to 3rd parties?) which it expects will pay off in 2011

- government incentive programs - tax breaks or grants reduce hefty upfront cost and shorten consumer payback; US govt on board to 2016 and Canadian government on fence (Canada is 15% of sales now) but likely to start replacement for cancelled ecoEnergy program

- foreign exchange - WFI operates in USD, including dividends to Canadians (though those are 100% eligible dividends for income tax reports); as CAD rises relative to USD that's bad for Canadian investor

- no sales only purchases within last year by both mgmt & directors; very quiet

- outstanding - ROE > 50% with no leverage at all (no long term debt at all)!; ROA close to 50%; operating margin 15+%, net margin 11+%; this is on level with the best of the best on the TSX (see this Sept.5 GlobeInvestor screen by Simon Avery for high ROE in large TSX stocks - only the TMX Group is up there with WFI); by comparison, a main competitor LSB Industries (NYSE: LXU) has ratios less than half as good and a large amount of debt (Debt/Equity = 0.7 in 2009)

- gross margins did fall 4% in 2Q10 (Aug.5) but mgmt stated in conf call they expect better in 2011

- absence of debt removes financial leverage effect > earnings & ROE will be much more stable i.e. risk is reduced

- inventories, receivables very stable

- 2Q2010 Earnings Call Podcast from Newswire.ca

- founding Shields family still owns about 25% of company shares, but in laudable and unusual fashion, has not created non- or restricted-voting share class

- managers and directors have significant stake in form of actual shares; no stock options outstanding as of Aug.5 > no temptation for accounting shenanigans

- WFI's competitors are in several cases owned by large corporations - some may want to "round out" their portfolio with a company that is a close second in market share, especially if market seems to be taking off and there is potential for massive sales increases

- WFI capital structure could easily take on some some debt since it has none at the moment - a big corp with debt could apply its own financial leverage to increase ROE even more since ROA at 50% is way above current borrowing costs

- big corp might have tax credits available from losses to shield income of WFI

- much as it is nice to receive dividends, WFI's dividend policy makes no sense - it should be paying zero dividends - if it can reinvest earnings at ROE 50+%

- big corp could apply its purchasing power to reduce material costs (WFI mentions this factor as an advantage its larger competitors have) and increase margins

- WFI's stock price is low compared to its reasonable value even under its present structure & operations

- due to very low trading volume, WFI stock price entails an illiquidity price penalty (as manifested in high bid-ask spread), probably quite substantial (10%?); a good part of the reason I believe is that it is a US company trading on the TSX

- minimum $29, using very conservative assumptions of - zero growth for the next two years, followed by a ten year period of 15% annual growth in earnings and dividends then a steady state of 5% annual growth thereafter, combined with a high market risk premium of 8% (over the risk free rate of 2%; one consideration was future likely available rates of return per this previous post); assumption of no growth based on the US housing market staying flat and housing starts not recovering for another two years, since that is the key to WFI's growth; assumption of 15% growth based on very limited penetration of geothermal and its compelling economic advantages to property owners, both residential and commercial, and the vast potential market, combined with the fact that WFI's annual growth in the period before the 2008 housing and market crash ranged from 15 to 60%; assumption of 5% constant growth thereafter accounts for most of the eventual total discounted cash flow value of WFI and is at the low end of historic corporate returns;

- assumption of 1.1 beta, not actually calculated in strict terms as the covariance with market return, implies higher volatility than the overall TSX, though one might wonder comparing the price chart of the two (along with LXU, WFI's main competitor) on Yahoo Finance; if beta is only 1, same as the market, the value of of WFI goes up a lot - to $62 for the optimistic assumptions and $34 under the conservative assumptions; the absence of any leverage / debt in WFI reduces operating and financial risk of WFI, stabilising earnings, and is a reason to think its market volatility should be less; reading through WFI's financial statements, one gets a feeling of squeaky clean and no nasty surprises in the offing (e.g. there has never been a big write-off of one-time charges, there are no off balance sheet obligations), which lessens the chances of downward price spikes

- up to $50 using reasonable but not outlandish assumptions - 2% growth for two years, in line with expected inflation, 20% for ten years, in line with resumption of a housing market back up to about 1 million US housing starts, up from half that today, along with normal credit conditions and 6% constant growth steady state afterwards

- growth is the key to WFI's value - the current earnings justify a stock price of $10 (12% discount rate) to $15 (8% discount rate); one to think this stock is worth more, one has to believe that geothermal is a coming thing and that WFI will be along for a very profitable ride

- working backwards from the implications of the current market price of around $25.50, the growth rates in WFI's earnings and dividends are modest (6 to 6.5%) even with high required rates of return of 10%; this looks quite achievable for this company

- the model I've used is the dividend discount model in three stages ( go to McGraw Hill's Investments textbook website to download the spreadsheet here)

- my assumptions, values tested and a look at the model

- WFI is currently trading a narrow band bouncing up and down daily from $25 to $26; if it continues to do so, the 3.5% dividend return provides some return

Last, and perhaps not least for many people, WFI is providing a nuts and bolts, highly effective energy solution that helps both consumers in a direct financial sense and the environment by reducing the need for non-renewable fuel. What's not to like about this company?

Disclosure: I now own some shares in WFI. I know, I know, it's not in keeping with my passive index fund investing strategy but after my best shot at due diligence, including especially establishing a value, I think it's worth an exception.

Disclaimer: This post is my opinion only as to how and why I came to my own investment decision. Whether you agree or not, it should not be taken as investment advice.

Stumble It!

Stumble It!

4 comments:

Good post. I think you made the right move (in buying this one).

Cheers!

Thanks for the support, FC, but the market seems to disagree with me as the price went down today!

Wondering if you still own this and still like it? It's comedown a little and I'm thinking of picking up some shares.

Hi pattirose,

Yes I still do own it. Still looks as though it is managing through the tough housing market, which may have another year or two to run. Not adding to my position, which is constrained by what I decided I would allocate to it within my portfolio, but if anything it is a better bargain than when I bought it. Will be listening to the conference call later today to see what they say about the higher taxes and the big inventory buildup (short term stuff) or anything significant for the longer term.

Post a Comment