The EDHEC-Risk Institute, an academic institute with a practical orientation, has put out a couple of papers that knock down some investment wishful thinking.

In Does Finance Theory Make the Case for Capitalisation-Weighted Indexing?, authors Felix Goltz and Véronique Le Sourd, after reviewing the academic literature, answer that question quite categorically - "No, it does not". A cap-weighted index does not represent the market portfolio of finance theory and even if it could, it would not be efficient in a risk-return sense without making highly unrealistic assumptions. As they say, "... from a theoretical perspective, cap-weighted stock market indices seem to offer no particular advantage". It then becomes a practical problem to construct indices that offer higher return to risk trade-off (as expressed in higher Sharpe ratios). They offer their own Efficient Indices here and when they assess alternatives (Improved Beta? A Comparison of Index Weighting Schemes) like fundamental indexing, equal weight indexing, efficient indexing and minimum volatility indexing, the alternatives all beat Cap-Weighting (e.g. their US Efficient Index has outperformed the FTSE US Cap-weighted index by 2% annually since 2002 while lowering volatility). Of course, not all these better indices are investable for the average retail investor - so far only fundamental and equal-weight funds are available - and the costs of running the index fund could obviate the benefits (witness the sorry story of mutual funds in Canada) if too high (my assessment of US ETFs suggests they do preserve the benefit in real life and I've started a realistic portfolio experiment for a Canadian investor that includes Canadian ETFs).

The other foray into clarifying reality vs wishful thinking is The Performance of Socially Responsible Investment and Sustainable Development in France: An Update after the Financial Crisis by Noël Amenc and Véronique Le Sourd (again! does she like setting people straight or what?). Comparing the performance of SRI funds in France, they cannot really find any significant difference with ordinary funds in terms of risk-return efficiency. During the period of the financial crisis, SRI funds provided no better protection against the downturn. A subset of SRI, Green (environmental) funds, compared to best-in-class ordinary funds "... reveals, over the long term, higher alpha for green funds, with higher risks, including higher extreme risks." The paper's findings will give some comfort to the SRI-minded investor with its evidence that the investor need not lose out by going SRI. However, it does also remind us that SRI is no investing philosophy panacea either. I am currently reading Confessions of a Radical Industrialist by Ray Anderson and he leaves an over-the-top impression that going green is a sure-fire route to greater profitability. That may be so if you do it right but I daresay there are well run and badly run SRI and green companies, just as in any human activity (as an illustration of the principle for those with a reflective bent, I highly recommend the book Albert Speer: His Battle With Truth by Gita Sereny; it tells the story of a highly intelligent but amoral organizational genius who put his talents in the service of evil as the mastermind of Hitler's war production machine)

Wednesday, 29 September 2010

Saturday, 25 September 2010

Index Investing Becoming a Victim of Its Own Success

Too much of a good thing can end up being bad. That includes using a benchmark index as the basis for an investing apparently.

In the July 2010 paper (download here from SSRN; acknowledgement to Stingy Investor where I found the link) On the Economic Costs of Index-Linked Investing, NYU prof and NBER research associate Jeffrey Wurgler reviews some research results that are disquieting for investors who follow a passive index strategy based on popular indices such as the S&P 500.

Wurgler says: "... the increasing popularity of index-linked investing may well be reducing its ability to deliver its advertised benefits ..." The problems:

What does he suggest one do about it?

In the July 2010 paper (download here from SSRN; acknowledgement to Stingy Investor where I found the link) On the Economic Costs of Index-Linked Investing, NYU prof and NBER research associate Jeffrey Wurgler reviews some research results that are disquieting for investors who follow a passive index strategy based on popular indices such as the S&P 500.

Wurgler says: "... the increasing popularity of index-linked investing may well be reducing its ability to deliver its advertised benefits ..." The problems:

- the inclusion of stocks in the index pushes up prices, by around 9% around the time of the event, a factor that has been getting worse as indexing has gained popularity; this effect is observed for other indices besides the S&P 500, like the TSX 300 (now the delicately named TSX Composite, which hides the fact the fact that it has been shrinking steadily in number of stocks over the years to 235 today)

- active managers who are benchmarked against the index have an incentive to overweight index members, even if they think a non-index stock will appreciate the same percentage, due to lesser tracking error

- stocks that join a leading index such as the S&P 500 suddenly begin to move much in tandem and keep doing so, which Wurgler vividly likens to the movements of a school of fish; he calls this effect "detachment"

- the S&P 500 school of fish members moves on their own and less like the overall market, a net loss of diversification for the investor

- S&P 500 membership has in the past over the long period of 1980 to 2005 conferred an increasing price premium; he cites one study that found the S&P 500 stocks got an 82 basis point annual alpha return premium; while it might seem like a good thing to get a hefty excess return, he says it might be a sign of an "indexing bubble" that will sooner or later deflate

- as a consequence, bubbles and crashes are more likely; he discusses the mechanism that may explain both the 1987 crash and the May 2010 flash crash

- the risk and return relationship actually does not hold - low beta(risk) stocks have been found to generate better returns, by a lot, than high beta stocks, a phenomenon he rightly calls a spectacular anomaly; he explains how fund managers benchmarked to an index will favour high beta stocks

- he raises the possibility that the S&P cap-weighted index amounts to a strategy of large-cap growth and momentum ... "Clearly, the line between passive and active investment is blurrier than usually presented."

What does he suggest one do about it?

- instead of the S&P 500, pick a broader index like the Wilshire 5000 - "The S&P 500 Index's detachment means, however, that it is reflecting less and less the performance of the full stock market. Index funds based on the more comprehensive Wilshire 5000 (which has included as many as 7,200 stocks) are now providing more robust diversification and stock market exposure."

- exploit the observed "spectacular anomaly" through strategies that focus on low-beta stocks, e.g. employ maximum Sharpe ratio, minimum volatility and absolute returns, though I'd guess that is probably beyond most individual investors' capability

Thursday, 23 September 2010

WaterFurnace Renewable Energy (TSX: WFI) - a Buy for all the right reasons

WaterFurnace Renewable Energy (TSX: WFI) is a very unusual company - unlike every other trendy "do good for the environment" stock, it is highly profitable and its stock is, I believe, much undervalued. Here's why.

Geothermal Heat PumpsWFI makes geothermal heat pumps. Wikipedia article describes history, principles that underlie the technology, how the technology works, economics. WFI's former president Bruce Ritchie explains in this video how it works and why it is so worthwhile.

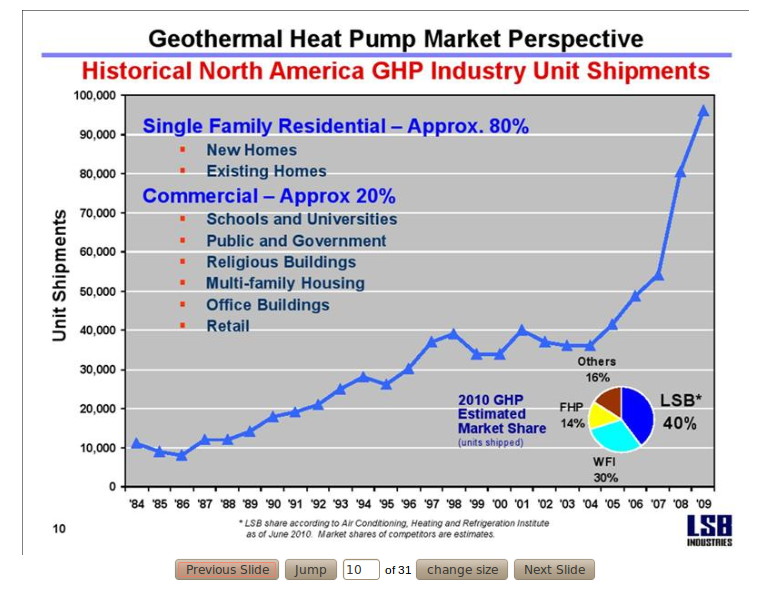

Industry Prospects

Presentation by LSB Industries at Canaccord Genuity Conference 10th August 2010

Geothermal Maturity

Market Growth:

Competition

WaterFurnace the Company and the Stock

Visibility: Not Just Under the Radar, It's Well Below Ground

Last, and perhaps not least for many people, WFI is providing a nuts and bolts, highly effective energy solution that helps both consumers in a direct financial sense and the environment by reducing the need for non-renewable fuel. What's not to like about this company?

Disclosure: I now own some shares in WFI. I know, I know, it's not in keeping with my passive index fund investing strategy but after my best shot at due diligence, including especially establishing a value, I think it's worth an exception.

Disclaimer: This post is my opinion only as to how and why I came to my own investment decision. Whether you agree or not, it should not be taken as investment advice.

Geothermal Heat PumpsWFI makes geothermal heat pumps. Wikipedia article describes history, principles that underlie the technology, how the technology works, economics. WFI's former president Bruce Ritchie explains in this video how it works and why it is so worthwhile.

Industry Prospects

Presentation by LSB Industries at Canaccord Genuity Conference 10th August 2010

Geothermal Maturity

- technology for energy known for many years, proven efficiency benefits; manufacturer equipment still improving but fairly close in technical capability - key differentiator for install success is contractor installer skill and diligence

- dealer networks in place, extension of capability for contractors

- consumer knowledge in North America in its infancy but the information/hype infrastructure is in place - industry associations (GeoExchange in USA, Canadian GeoExchange Coalition), web sites and consumer forums (GreenBuilding Talk)

- residential easiest and cheapest for new-build but still attractive for retrofit, esp. at furnace or air con replacement moment; WatwerFurnace claims present 100k annual install rate could rise to 1 million p.a. by 2016

- attraction is fuel bill savings, appreciable now and probably greater in future if commercial aka power company prices rise

- government tax breaks and write-offs are an incentive

- substantial up-front cost creates affordability challenge, especially at a time when home values are dropping, credit is tight and consumers are trying to reduce debt, not take on more

- lack of knowledge and solution visibility and trust not quite there - are we close to a tipping point?

Market Growth:

- stalled during housing crash in USA - housing starts down to 500k annually but WaterFurnace expecting (Q2 earnings call) return to 1.2 -1.5 million p.a. by c. 2012

Competition

- main competitor is LSB Industries (NYSE: LXU), which has about twice the $ sales of WFI in climate control, though the manufacturing figures of the US Energy Information Administration for 2008 has them about equal in shipments (WFI = Indiana, LXU = Oklahoma); WFI has gained market share in 2010, as it claims in its 2Q Report - its sales rose 13% in the first six months of 2010 while LXU's fell 11%;

- biggest other competition - Trane (owner Ingersoll Rand), Florida Heat Pump (owner Bosch), McQuay (owner Daikin of Japan), Mammoth (private company)

- October release of shipment figures by the US EIA will show evolution of market share through 2009

WaterFurnace the Company and the Stock

Visibility: Not Just Under the Radar, It's Well Below Ground

- Low trading volume - 11,000 average but in recent months even lower; trades are in small amounts, 1 or 2 board lots at a time, indicating retail investors, not institutional investors are the market

- Google Finance does not even track price now - trading volumes too low?

- Only two analysts cover it

- Only a few Globe and Mail stories - mostly in stock screens results for desirable traits

- US interest low - likely because it is a US company traded in Canada on TSX

- not listed in StockChase, no chat board on Raging Bull etc

- no search results on book website for Clean Tech Revolution, nor is it mentioned in the book; not in book Investing in Renewable Energy nor is it in a search of that book's website Green Chip Stocks

- boring - uggh, they make HVAC equipment; ughh, stock price hasn't budged in four years; also likely means that "momentum" traders are staying away, so we shouldn't expect big leaps and swings; boring is good

- Cormark Securities has a full stock investment assessment on Power and Alternative Energy Companies that includes WaterFurnace; 12 mth price target is C$31 based on historical average P/E and projected EPS in 2011

- warranty costs - WFI mgmt assumes constant failure rate according to historical experience; has a long enough track record to assess the 10 year warranty it offers but new products may not do as well (any ISO quality control for manufacturing or by its chosen supplier partners?)

- margin pressure due to

- material costs, esp copper tubing, rising faster than price increase can compensate, together with

- competitors, who are in most cases, as Company docs say, larger and can source raw materials cheaper; 2Q earnings call mentioned drive to expand market share as successful but at cost of lower margins; same call mentions that it has taken steps to improve efficiency (outsource some manuf to 3rd parties?) which it expects will pay off in 2011

- government incentive programs - tax breaks or grants reduce hefty upfront cost and shorten consumer payback; US govt on board to 2016 and Canadian government on fence (Canada is 15% of sales now) but likely to start replacement for cancelled ecoEnergy program

- foreign exchange - WFI operates in USD, including dividends to Canadians (though those are 100% eligible dividends for income tax reports); as CAD rises relative to USD that's bad for Canadian investor

- no sales only purchases within last year by both mgmt & directors; very quiet

- outstanding - ROE > 50% with no leverage at all (no long term debt at all)!; ROA close to 50%; operating margin 15+%, net margin 11+%; this is on level with the best of the best on the TSX (see this Sept.5 GlobeInvestor screen by Simon Avery for high ROE in large TSX stocks - only the TMX Group is up there with WFI); by comparison, a main competitor LSB Industries (NYSE: LXU) has ratios less than half as good and a large amount of debt (Debt/Equity = 0.7 in 2009)

- gross margins did fall 4% in 2Q10 (Aug.5) but mgmt stated in conf call they expect better in 2011

- absence of debt removes financial leverage effect > earnings & ROE will be much more stable i.e. risk is reduced

- inventories, receivables very stable

- 2Q2010 Earnings Call Podcast from Newswire.ca

- founding Shields family still owns about 25% of company shares, but in laudable and unusual fashion, has not created non- or restricted-voting share class

- managers and directors have significant stake in form of actual shares; no stock options outstanding as of Aug.5 > no temptation for accounting shenanigans

- WFI's competitors are in several cases owned by large corporations - some may want to "round out" their portfolio with a company that is a close second in market share, especially if market seems to be taking off and there is potential for massive sales increases

- WFI capital structure could easily take on some some debt since it has none at the moment - a big corp with debt could apply its own financial leverage to increase ROE even more since ROA at 50% is way above current borrowing costs

- big corp might have tax credits available from losses to shield income of WFI

- much as it is nice to receive dividends, WFI's dividend policy makes no sense - it should be paying zero dividends - if it can reinvest earnings at ROE 50+%

- big corp could apply its purchasing power to reduce material costs (WFI mentions this factor as an advantage its larger competitors have) and increase margins

- WFI's stock price is low compared to its reasonable value even under its present structure & operations

- due to very low trading volume, WFI stock price entails an illiquidity price penalty (as manifested in high bid-ask spread), probably quite substantial (10%?); a good part of the reason I believe is that it is a US company trading on the TSX

- minimum $29, using very conservative assumptions of - zero growth for the next two years, followed by a ten year period of 15% annual growth in earnings and dividends then a steady state of 5% annual growth thereafter, combined with a high market risk premium of 8% (over the risk free rate of 2%; one consideration was future likely available rates of return per this previous post); assumption of no growth based on the US housing market staying flat and housing starts not recovering for another two years, since that is the key to WFI's growth; assumption of 15% growth based on very limited penetration of geothermal and its compelling economic advantages to property owners, both residential and commercial, and the vast potential market, combined with the fact that WFI's annual growth in the period before the 2008 housing and market crash ranged from 15 to 60%; assumption of 5% constant growth thereafter accounts for most of the eventual total discounted cash flow value of WFI and is at the low end of historic corporate returns;

- assumption of 1.1 beta, not actually calculated in strict terms as the covariance with market return, implies higher volatility than the overall TSX, though one might wonder comparing the price chart of the two (along with LXU, WFI's main competitor) on Yahoo Finance; if beta is only 1, same as the market, the value of of WFI goes up a lot - to $62 for the optimistic assumptions and $34 under the conservative assumptions; the absence of any leverage / debt in WFI reduces operating and financial risk of WFI, stabilising earnings, and is a reason to think its market volatility should be less; reading through WFI's financial statements, one gets a feeling of squeaky clean and no nasty surprises in the offing (e.g. there has never been a big write-off of one-time charges, there are no off balance sheet obligations), which lessens the chances of downward price spikes

- up to $50 using reasonable but not outlandish assumptions - 2% growth for two years, in line with expected inflation, 20% for ten years, in line with resumption of a housing market back up to about 1 million US housing starts, up from half that today, along with normal credit conditions and 6% constant growth steady state afterwards

- growth is the key to WFI's value - the current earnings justify a stock price of $10 (12% discount rate) to $15 (8% discount rate); one to think this stock is worth more, one has to believe that geothermal is a coming thing and that WFI will be along for a very profitable ride

- working backwards from the implications of the current market price of around $25.50, the growth rates in WFI's earnings and dividends are modest (6 to 6.5%) even with high required rates of return of 10%; this looks quite achievable for this company

- the model I've used is the dividend discount model in three stages ( go to McGraw Hill's Investments textbook website to download the spreadsheet here)

- my assumptions, values tested and a look at the model

- WFI is currently trading a narrow band bouncing up and down daily from $25 to $26; if it continues to do so, the 3.5% dividend return provides some return

Last, and perhaps not least for many people, WFI is providing a nuts and bolts, highly effective energy solution that helps both consumers in a direct financial sense and the environment by reducing the need for non-renewable fuel. What's not to like about this company?

Disclosure: I now own some shares in WFI. I know, I know, it's not in keeping with my passive index fund investing strategy but after my best shot at due diligence, including especially establishing a value, I think it's worth an exception.

Disclaimer: This post is my opinion only as to how and why I came to my own investment decision. Whether you agree or not, it should not be taken as investment advice.

Thursday, 16 September 2010

Canada Falling Back in World University Rankings

The Times World University Rankings for 2010 are out and it is not good news for Canada.

Last year 11 Canadian universities were amongst the top 200 ranked universities in the world. This year only 9 made the list, which uses a supposedly improved methodology that puts less weight on reputation and more on more measurable harder facts. A bunch got dropped and a couple of new names entered the top 200 from Canada. The list:

Those who are fond of knocking the USA or predicting its imminent fall may wish to consider that the new rankings indicate an overwhelming dominance by that country in higher education. It dominates in every way: owning the top 5 spots, 7 of the top 10, 27 of the top 50 and 72 of the top 200. That's 18 more in the top 200 than last year! One negative mentioned in this analysis article is that public universities like the U. of California system are suffering from government cutbacks as a result of the debt crisis. Rich private universities like world no.1 Harvard are merely less rich.

The UK has held its own with 29 spots in the top 200, the same as last year and it has the other three in the top ten.

Though Canada's position has fallen back relative to the best, I would not want to be a citizen of much larger countries than Canada that have fared very poorly in these rankings such as Japan with only 5 spots, France with 4, and Italy with not a single university among the top 200. In the national "medals table" (see here) Canada is 5th after the USA, the UK, Germany and the Netherlands.

Amongst countries of the emerging world, China is already in the top class - including Hong Kong and Mainland China together, it would be tied at 10 spots with the Netherlands. The other members of the BRIC - Brazil, Russia and India - do not have a single top 200 university, though the Times editors feel India is on track to muscle into it soon, while Russia is in decline. It is an interesting thought relative to investment prospects for these countries given the key role universities play in economic development.

There is competition not just amongst universities, but between rankings too. After a combined effort in 2009 (the one which is used above to compare), QS and Times have split. The QS 2010 Rankings paint a slightly different overall picture, though Canada has also fallen back in this set of rankings. There is one less top 200 spot - SFU has slipped down to 216th and all but one (U of T) have slipped lower. In QS' results, the number one spot is held by Cambridge, the UK has 4 of the top ten, the US has fewer overall in the top 200, only 53 total, which is down one from last year.

The QS rankings are interesting in that they go right down to the top 500. Being down there is not so shabby, even for bottom-feeders like Carleton, Concordia and U du Québec considering that there are said to be more than 17,000 universities around the world.

Last year 11 Canadian universities were amongst the top 200 ranked universities in the world. This year only 9 made the list, which uses a supposedly improved methodology that puts less weight on reputation and more on more measurable harder facts. A bunch got dropped and a couple of new names entered the top 200 from Canada. The list:

- U of Toronto - 17th place in the world - up from 29th!

- UBC - 30th - up ten spots too from 40th!

- McGill - 35th - down from 18th ;-(

- McMaster - 93rd up fifty spots from 143rd!!

- U of Alberta - 127th, down from 59th, ouch!

- U of Victoria - 130th, from nowhere last year!!!

- U of Montreal - 138th vs 107th

- Dalhousie - 193rd, another new entrant

- SFU - 199th, still hanging on after 196th placing last year

Those who are fond of knocking the USA or predicting its imminent fall may wish to consider that the new rankings indicate an overwhelming dominance by that country in higher education. It dominates in every way: owning the top 5 spots, 7 of the top 10, 27 of the top 50 and 72 of the top 200. That's 18 more in the top 200 than last year! One negative mentioned in this analysis article is that public universities like the U. of California system are suffering from government cutbacks as a result of the debt crisis. Rich private universities like world no.1 Harvard are merely less rich.

The UK has held its own with 29 spots in the top 200, the same as last year and it has the other three in the top ten.

Though Canada's position has fallen back relative to the best, I would not want to be a citizen of much larger countries than Canada that have fared very poorly in these rankings such as Japan with only 5 spots, France with 4, and Italy with not a single university among the top 200. In the national "medals table" (see here) Canada is 5th after the USA, the UK, Germany and the Netherlands.

Amongst countries of the emerging world, China is already in the top class - including Hong Kong and Mainland China together, it would be tied at 10 spots with the Netherlands. The other members of the BRIC - Brazil, Russia and India - do not have a single top 200 university, though the Times editors feel India is on track to muscle into it soon, while Russia is in decline. It is an interesting thought relative to investment prospects for these countries given the key role universities play in economic development.

There is competition not just amongst universities, but between rankings too. After a combined effort in 2009 (the one which is used above to compare), QS and Times have split. The QS 2010 Rankings paint a slightly different overall picture, though Canada has also fallen back in this set of rankings. There is one less top 200 spot - SFU has slipped down to 216th and all but one (U of T) have slipped lower. In QS' results, the number one spot is held by Cambridge, the UK has 4 of the top ten, the US has fewer overall in the top 200, only 53 total, which is down one from last year.

The QS rankings are interesting in that they go right down to the top 500. Being down there is not so shabby, even for bottom-feeders like Carleton, Concordia and U du Québec considering that there are said to be more than 17,000 universities around the world.

Monday, 13 September 2010

TD Waterhouse Offers International Trading - Partly Good, Partly Bad

The news that TD Waterhouse (hat tip to Wealthy Boomer Jonathan Chevreau's post today) is offering the ability to trade directly on major international stock exchanges is mostly good - international diversification becomes a little easier. Canada is catching up to the UK, where TDW has offered such a service for years now.

I guess the small matter of the financial crash of 2008 somewhat delayed the implementation of TDW's intention announced by the Globe and Mails's Rob Carrick as I posted about two years ago, almost to the day.

But TDW is charging too much. Why is TDW charging Canadians £29 commission per trade (see TDW Canada Online Commissions and Fees) for buying shares in the UK when TDW UK's commission is less than half at £12.50 (rate table here)? The same higher cost applies to the other foreign markets too. Give us a break TDW!

Update Sept.16: TDW says blandly in an email reply to my enquiry that the higher commission fees in Canada are "...reflective of the greater underlying costs..." and that they are "competitive". I guess the Canadian operation of TDW isn't as efficient as it is in the UK. TDW also says the online Global Trading capability cannot be used in registered accounts, another difference with the UK where it is possible to trade on international exchanges in the similar ISA account.

I guess the small matter of the financial crash of 2008 somewhat delayed the implementation of TDW's intention announced by the Globe and Mails's Rob Carrick as I posted about two years ago, almost to the day.

But TDW is charging too much. Why is TDW charging Canadians £29 commission per trade (see TDW Canada Online Commissions and Fees) for buying shares in the UK when TDW UK's commission is less than half at £12.50 (rate table here)? The same higher cost applies to the other foreign markets too. Give us a break TDW!

Update Sept.16: TDW says blandly in an email reply to my enquiry that the higher commission fees in Canada are "...reflective of the greater underlying costs..." and that they are "competitive". I guess the Canadian operation of TDW isn't as efficient as it is in the UK. TDW also says the online Global Trading capability cannot be used in registered accounts, another difference with the UK where it is possible to trade on international exchanges in the similar ISA account.

Monday, 6 September 2010

Investment Banks and Hedge Funds: the Bubble of the Past Quarter Century?

The Credit Bubble leading to the Crash of 2008. Who profited and where did all the money go? That's a question I have been asking myself since 2007 and the start of the credit / financial crisis. The answer I now believe is a) employees of investment banking; b) managers / employees of hedge funds; c) shareholders with stakes (i.e. whether as separate entities or whose profits flow up to a parent entity) in investment banking and hedge funds.

The Evidence: Read Baseline Scenario's Good for Goldman and Paper of the Year (hat tip to the Awl for the link) along with the April 15, 2010 speech by European Central Bank member of the Executive Board Lorenzo Bini Smaghi. The sources give stats and graphs showing that since around the mid 1980s employee compensation in these businesses has risen steadily far faster than any measure of education, risks or productivity would explain till it is around 40% more than it should be. This did not happen in the traditional banking side of things, only in investment banking and hedge funds. Smaghi says: "It is important to note that this is not due to rising compensation in “traditional” financial sectors like credit and insurance, but due to the large increase in compensation in non-traditional financial activities like investment banks, hedge funds and the like."

In addition, financial industry growth has taken an even larger share of GDP. Here is a fascinating graph showing US data from Research Affiliates LLC (reproduced with their permission - and thanks to blogger Preet Banerjee of WhereDoesAllMyMoneyGo.com for arranging this; the slide is also available as part of the Claymore-produced slide presentation Fundamental vs Traditional Index Investing on the Advisor.ca website - N.B. I have added to Research Affiliate's chart the red Bubble line)

The Fundamental Index Methodology used by Research Affiliates is built using four accounting measures of sector size to weight the index - sales, income, dividends and book value. It thus reflects the long term growth of the Financial Services sector in achieving actual results. Unlike the infamous Tech bubble of 2000, which was reflected in the brief spike of unrealistic share prices shown in the market cap weighted index on the left side of the slide, the Financial Services bubble has been building for decades. It has been made up of real sales, real profits and real dividends flowing to real companies and people.

When exactly did the Financial Services secular bubble start? That's a bit hard to tell, since as Smaghi discusses, the growth of Financial Services is a good thing up to a point since there is more efficient allocation of savings to capital investment and faster economic growth. But beyond a certain point, which he says the financial sector certainly surpassed, the excessive risk-taking and unproductive allocation cause bubbles and crashes, like the Tech bubble itself. "... excessive rents reaped by the financial industry lead to increased risk-taking which can endogenously generate boom and bust episodes..." Thus the expansion of financial services since the 1960s has not been all bubble, some of it has been beneficial.

I've drawn my Bubble line at the point in the late 1980s when salaries began their vertiginous ascent (see Fig.2 of Smaghi's attachments in this pdf), a point at which there is also a sudden higher rate of increase in the share of financial services in the Fundamental Index (i.e. when they started to make gobs of money) in the above chart.

What is the right size for Financial Services and where will the sector settle out?

It is more or less universally agreed that the Financial services sector is too big. The shrinkage has already started. The Fundamentals show it - note the shrinkage in sector size from 2007 onwards in the above chart. Markets expect it too - note a much bigger change in share in the above chart. This difference between the trailing results-influenced Fundamental Index and Market Cap Indices shows up in popular ETFs:

Lorenzo Bini Smaghi: "...we still run into practical problems if we try to establish the right “threshold”[size of the financial sector], and research in this field has been very limited".

And there is lots of expert debate and disagreement about how to go about it (e.g. William Buiter at FT.com, others at FT.com, Smaghi's review of options), never mind the sometimes politically-motivated actions of governments (e.g. punitive revenge-seeking laws, which though perfectly justified in my opinion, they don't necessarily help the individual investor make money / avoid losing more).

It looks as though one measure sure to come is higher capital requirements of banks per the Financial Post. How much that will constrain the size of the financial sector is very hard to predict.

Investing Implications

When Larry MacDonald says he would be leery of investing in the US financial sector except for Goldman Sachs, maybe he's right. But the US financial sector has the lowest share compared to any major world index so maybe the market has already anticipated and priced in the effect of regulation-imposed slimming. Maybe it has even over-reacted, as can happen in crashes after bubbles. If the market has over-reacted, the Fundamental Index may still be closer to the eventual settling point than the market-cap index.

Lately the Canadian banks, who on the face of it have the most out-of-line highest proportion of the total stock market amongst Fundamental indices anywhere, and thus might be the most likely candidates for regulatory reduction, seem only somewhat likely to be heading towards shrinkage. Finance Minister Flaherty has publicly resisted calls for additional bank taxes (see the Toronto Star back in April). All five major Canadian banks are ranked among the Top 50 Safest Banks in the World and all 5 in the Top 10 for North America by Global Finance. And the proposed capital ratios mentioned in the Financial Post report are well within existing levels at all the major Canadian banks. Some are even talking of re-instituting dividend increases (see speculation on MoneyEnergy and in the Financial Post's Dividend hikes expected from National Bank, then Scotia and TD) so maybe it is a case that strong Canadian banks, already getting a significant chunk of their business outside Canada, are ready to expand into a shrinking less competitive sector beyond Canada's borders.

Bottom line: as an index investor with holdings in the Fundamental-weighted Index Funds like PXF, CRQ and PRF, I may be at slightly higher risk than Cap-weight investors in North America if the share of financial services is destined to return to pre-bubble days of 1986. I believe there is an appreciably higher risk for the non-North American Rest-of-the-Developed World (PXF). For now, I am not changing my portfolio strategy away from Fundamental Indexing to Market-Cap Indexing. Time will tell.

The Evidence: Read Baseline Scenario's Good for Goldman and Paper of the Year (hat tip to the Awl for the link) along with the April 15, 2010 speech by European Central Bank member of the Executive Board Lorenzo Bini Smaghi. The sources give stats and graphs showing that since around the mid 1980s employee compensation in these businesses has risen steadily far faster than any measure of education, risks or productivity would explain till it is around 40% more than it should be. This did not happen in the traditional banking side of things, only in investment banking and hedge funds. Smaghi says: "It is important to note that this is not due to rising compensation in “traditional” financial sectors like credit and insurance, but due to the large increase in compensation in non-traditional financial activities like investment banks, hedge funds and the like."

In addition, financial industry growth has taken an even larger share of GDP. Here is a fascinating graph showing US data from Research Affiliates LLC (reproduced with their permission - and thanks to blogger Preet Banerjee of WhereDoesAllMyMoneyGo.com for arranging this; the slide is also available as part of the Claymore-produced slide presentation Fundamental vs Traditional Index Investing on the Advisor.ca website - N.B. I have added to Research Affiliate's chart the red Bubble line)

The Fundamental Index Methodology used by Research Affiliates is built using four accounting measures of sector size to weight the index - sales, income, dividends and book value. It thus reflects the long term growth of the Financial Services sector in achieving actual results. Unlike the infamous Tech bubble of 2000, which was reflected in the brief spike of unrealistic share prices shown in the market cap weighted index on the left side of the slide, the Financial Services bubble has been building for decades. It has been made up of real sales, real profits and real dividends flowing to real companies and people.

When exactly did the Financial Services secular bubble start? That's a bit hard to tell, since as Smaghi discusses, the growth of Financial Services is a good thing up to a point since there is more efficient allocation of savings to capital investment and faster economic growth. But beyond a certain point, which he says the financial sector certainly surpassed, the excessive risk-taking and unproductive allocation cause bubbles and crashes, like the Tech bubble itself. "... excessive rents reaped by the financial industry lead to increased risk-taking which can endogenously generate boom and bust episodes..." Thus the expansion of financial services since the 1960s has not been all bubble, some of it has been beneficial.

I've drawn my Bubble line at the point in the late 1980s when salaries began their vertiginous ascent (see Fig.2 of Smaghi's attachments in this pdf), a point at which there is also a sudden higher rate of increase in the share of financial services in the Fundamental Index (i.e. when they started to make gobs of money) in the above chart.

What is the right size for Financial Services and where will the sector settle out?

It is more or less universally agreed that the Financial services sector is too big. The shrinkage has already started. The Fundamentals show it - note the shrinkage in sector size from 2007 onwards in the above chart. Markets expect it too - note a much bigger change in share in the above chart. This difference between the trailing results-influenced Fundamental Index and Market Cap Indices shows up in popular ETFs:

- USA - in Vanguard's Market Cap VTI, Financial Services = 16.4% as of 31 July 2010 vs Powershares RAFI PRF = 20.9% as of 31 Aug 2010

- Canada - iShares TSX Composite XIC = 29.6% vs Claymore Canadian Fundamental Index CRQ = 45% as of 3 Sep 2010

- World - Vanguard All-World ex-US VEU = 25.8% as of 30 April vs PowerShares Developed RAFI ex-US PXF = 28.9% as of 3 Sep 2010

Lorenzo Bini Smaghi: "...we still run into practical problems if we try to establish the right “threshold”[size of the financial sector], and research in this field has been very limited".

And there is lots of expert debate and disagreement about how to go about it (e.g. William Buiter at FT.com, others at FT.com, Smaghi's review of options), never mind the sometimes politically-motivated actions of governments (e.g. punitive revenge-seeking laws, which though perfectly justified in my opinion, they don't necessarily help the individual investor make money / avoid losing more).

It looks as though one measure sure to come is higher capital requirements of banks per the Financial Post. How much that will constrain the size of the financial sector is very hard to predict.

Investing Implications

When Larry MacDonald says he would be leery of investing in the US financial sector except for Goldman Sachs, maybe he's right. But the US financial sector has the lowest share compared to any major world index so maybe the market has already anticipated and priced in the effect of regulation-imposed slimming. Maybe it has even over-reacted, as can happen in crashes after bubbles. If the market has over-reacted, the Fundamental Index may still be closer to the eventual settling point than the market-cap index.

Lately the Canadian banks, who on the face of it have the most out-of-line highest proportion of the total stock market amongst Fundamental indices anywhere, and thus might be the most likely candidates for regulatory reduction, seem only somewhat likely to be heading towards shrinkage. Finance Minister Flaherty has publicly resisted calls for additional bank taxes (see the Toronto Star back in April). All five major Canadian banks are ranked among the Top 50 Safest Banks in the World and all 5 in the Top 10 for North America by Global Finance. And the proposed capital ratios mentioned in the Financial Post report are well within existing levels at all the major Canadian banks. Some are even talking of re-instituting dividend increases (see speculation on MoneyEnergy and in the Financial Post's Dividend hikes expected from National Bank, then Scotia and TD) so maybe it is a case that strong Canadian banks, already getting a significant chunk of their business outside Canada, are ready to expand into a shrinking less competitive sector beyond Canada's borders.

Bottom line: as an index investor with holdings in the Fundamental-weighted Index Funds like PXF, CRQ and PRF, I may be at slightly higher risk than Cap-weight investors in North America if the share of financial services is destined to return to pre-bubble days of 1986. I believe there is an appreciably higher risk for the non-North American Rest-of-the-Developed World (PXF). For now, I am not changing my portfolio strategy away from Fundamental Indexing to Market-Cap Indexing. Time will tell.

Friday, 3 September 2010

iShares XTR Changes from Passive to Active

The steady disappearance of the income trust sector as a result of the looming 2011 federal tax change has forced iShares' hand in an interesting way regarding the now formerly-named iShares Income Trust Index Fund (symbol: XTR). Following a shareholder vote (press release here), the fund's name, strategy and investment objective have changed fairly radically - from passive index tracking of income trusts to active management of any and all income bearing investments under the new title iShares Diversified Monthly Income Fund.

As significant as the change is a non-change - the management fee will remain at 0.55% including, as the press release takes pains to point out, any embedded fees arising from XTR owning other ETFs. Though there probably will be higher costs for XTR shareholders (which we will be able to find out only later when annual reports are issued) from more frequent trading due to active management, I find it refreshing that active management will in this case be associated with low fees, a situation found all-too seldom in Canada. I hope that the modified presence of XTR as a reasonable size fund ($200 million in assets) within the leading ETF provider puts some pressure for change to lower fees in the Canadian fund industry. Maybe the low fee will in itself be good to control excessive trading by XTR portfolio managers - they won't get paid much so why would they bother spending a lot of time on it and as we all know, excessive trading lowers returns.

It looks as though XTR is changing into a fund of funds since it will "... invest primarily in income-bearing Canadian iShares Funds". There may be duplication or overlap with its own iShares Conservative Core Portfolio Builder Fund (symbol XCR, MER 0.60%). As of September 2nd, the XTR fund holdings have not changed away from income trusts so I'll have to check back in a month when Blackrock says it will have completed the changeover to see how alike XTR and XCR may be. XCR is so small, with only $8 million in assets, that maybe they should just fold XCR into XTR.

As significant as the change is a non-change - the management fee will remain at 0.55% including, as the press release takes pains to point out, any embedded fees arising from XTR owning other ETFs. Though there probably will be higher costs for XTR shareholders (which we will be able to find out only later when annual reports are issued) from more frequent trading due to active management, I find it refreshing that active management will in this case be associated with low fees, a situation found all-too seldom in Canada. I hope that the modified presence of XTR as a reasonable size fund ($200 million in assets) within the leading ETF provider puts some pressure for change to lower fees in the Canadian fund industry. Maybe the low fee will in itself be good to control excessive trading by XTR portfolio managers - they won't get paid much so why would they bother spending a lot of time on it and as we all know, excessive trading lowers returns.

It looks as though XTR is changing into a fund of funds since it will "... invest primarily in income-bearing Canadian iShares Funds". There may be duplication or overlap with its own iShares Conservative Core Portfolio Builder Fund (symbol XCR, MER 0.60%). As of September 2nd, the XTR fund holdings have not changed away from income trusts so I'll have to check back in a month when Blackrock says it will have completed the changeover to see how alike XTR and XCR may be. XCR is so small, with only $8 million in assets, that maybe they should just fold XCR into XTR.

Wednesday, 1 September 2010

The S&P TSX 60 Index vs Claymore Canadian Fundamental ETF and Active Stock Picking

Take a look at the holdings of the supposedly passive iShares S&P TSX 60 Index ETF (symbol: XIU) and you will not find a number of companies that I would expect to see based on the philosophy of not actively selecting stocks but simply mimicking the overall stock market according to relative market value or capitalisation. The description of XIU on the iShares website says "The Index is comprised of 60 of the largest (by market capitalization) and most liquid securities listed on the TSX ...". Go into GlobeInvestor, do a stock search of all common stocks, then sort by the handy Market Cap column heading, compare the top 60 there with the XIU holdings and you are in for a surprise.

Missing from XIU are no less than eight stocks listed on the TSX amongst the 60 largest by market cap according to GlobeInvestor as of close of business September 1st:

That's why such small companies as Inmet Mining and Yellow Pages Income Fund, neither in even in the top 100 by market cap, show up in the 60 Index.

In contrast, another ETF which weights its stocks by size according to fundamental economic factors, the Claymore Canadian Fundamental Index ETF (symbol CRQ), has a substantially larger allocation to financial services - about 45% lately.

For an investor seeking to mirror the sector weighting of the overall Canadian economy, XIU comes closer than CRQ, since Financial services (including two other sectors - Real Estate and Management) make up only 20% of Canadian GDP (2008 figures - see Industry Canada data here).

The fact that CRQ's weighting scheme is based on actual historical accounting data, i.e. hard numbers, shows to what extent publicly-traded stocks in Canada are comprised of the financial industry. Private companies must thus make up a disproportionate share of other economic sectors. The Canadian public market is lop-sided.

For an investor seeking to go where the money is, or has been in the recent past, in terms of dividends, cash flow, sales and book equity, then CRQ comes closer than XIU since that is the basis on which CRQ picks stocks.

But to say that XIU is a totally passive fund, which therefore conforms best to an ideal, is not really true. XIU is not inherently superior to CRQ. Choosing XIU or CRQ comes down to which alternative investment strategy works best - XIU's strategy being based loosely on market cap (which in turn is based on the market's opinion of relative future value) and CRQ's based on past results being maintained in future. Which strategy works best is a matter of practical investigation.

Addendum

Just finished a chat with a very pleasant gentleman at S&P Canada who said that the financial companies in the above list were indeed excluded to keep the financial sector weight in line with the TSX Composite Index. Three others - Newmont, Boliden and Domtar - are not Canadian companies, a criteria which also forms part of the index composition. The last, Ivanhoe, has too small a float. iShares needs to improve its inaccurate summary description to include the fact that aligning to Composite sector weights is a criteria and that only Canadian registered companies, not merely TSX-listed companies, are included in the S&P TSX 60 / XIU.

Missing from XIU are no less than eight stocks listed on the TSX amongst the 60 largest by market cap according to GlobeInvestor as of close of business September 1st:

- Newmont Mining (symbol: NMC) in 13th spot by market cap

- Great West Lifeco (GWO) 18th,

- Power Financial (PWF) 28th

- Boliden AB (BLS) 29th

- Domtar Canada Paper (UFX - that's what GlobeInvestor says, though maybe it should be UFS) 32nd

- IGM Financial (IGM) 45th

- Ivanhoe Mines (IVN) 51st

- Fairfax Financial (FFH) 52nd

That's why such small companies as Inmet Mining and Yellow Pages Income Fund, neither in even in the top 100 by market cap, show up in the 60 Index.

In contrast, another ETF which weights its stocks by size according to fundamental economic factors, the Claymore Canadian Fundamental Index ETF (symbol CRQ), has a substantially larger allocation to financial services - about 45% lately.

For an investor seeking to mirror the sector weighting of the overall Canadian economy, XIU comes closer than CRQ, since Financial services (including two other sectors - Real Estate and Management) make up only 20% of Canadian GDP (2008 figures - see Industry Canada data here).

The fact that CRQ's weighting scheme is based on actual historical accounting data, i.e. hard numbers, shows to what extent publicly-traded stocks in Canada are comprised of the financial industry. Private companies must thus make up a disproportionate share of other economic sectors. The Canadian public market is lop-sided.

For an investor seeking to go where the money is, or has been in the recent past, in terms of dividends, cash flow, sales and book equity, then CRQ comes closer than XIU since that is the basis on which CRQ picks stocks.

But to say that XIU is a totally passive fund, which therefore conforms best to an ideal, is not really true. XIU is not inherently superior to CRQ. Choosing XIU or CRQ comes down to which alternative investment strategy works best - XIU's strategy being based loosely on market cap (which in turn is based on the market's opinion of relative future value) and CRQ's based on past results being maintained in future. Which strategy works best is a matter of practical investigation.

Addendum

Just finished a chat with a very pleasant gentleman at S&P Canada who said that the financial companies in the above list were indeed excluded to keep the financial sector weight in line with the TSX Composite Index. Three others - Newmont, Boliden and Domtar - are not Canadian companies, a criteria which also forms part of the index composition. The last, Ivanhoe, has too small a float. iShares needs to improve its inaccurate summary description to include the fact that aligning to Composite sector weights is a criteria and that only Canadian registered companies, not merely TSX-listed companies, are included in the S&P TSX 60 / XIU.

Subscribe to:

Comments (Atom)

Stumble It!

Stumble It!